Understanding Form GST ITC-03: Reversal of Input Tax Credit on Stock and Capital Goods

Understanding Form GST ITC-03: Reversal of Input Tax Credit on Stock and Capital Goods

In the Goods and Services Tax (GST) framework, Input Tax Credit (ITC) is a powerful mechanism that prevents the cascading effect of taxes. However, there are specific scenarios where ITC previously claimed must be paid back or reversed to the government. This compliance requirement is executed by filing Form GST ITC-03.

If you are a taxpayer transitioning from the regular tax scheme to the composition scheme, or if your supplied goods or services have recently been declared exempt, filing Form GST ITC-03 is a mandatory legal step.

What is Form GST ITC-03?

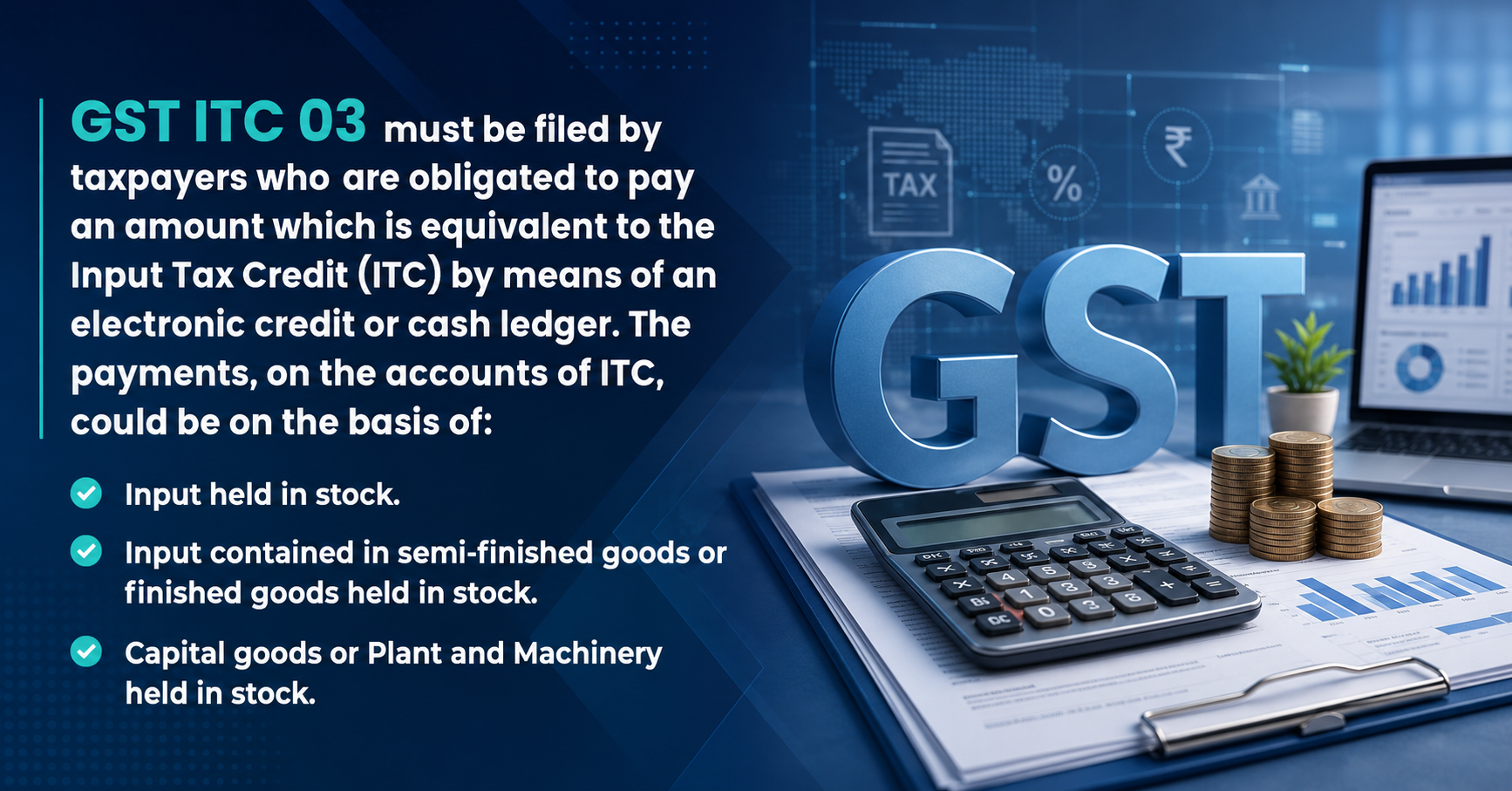

GST ITC-03 must be filed by taxpayers who are obligated to pay an amount equivalent to the Input Tax Credit (ITC) they have availed. This payment is made by debiting either the electronic credit ledger or the electronic cash ledger.

Essentially, it acts as a mechanism to return the tax credit to the tax department when the underlying goods change status from "taxable" to "exempt" or when your registration status changes.

When is Form GST ITC-03 Required?

The payments, on the account of ITC reversals under this form, could be triggered based on three main categories of inventory:

-

Input Held in Stock: Raw materials or traded goods lying in your warehouse or store that haven't been utilized yet.

Need help with this? Talk to Taxottam → -

Input Contained in Semi-Finished or Finished Goods Held in Stock: Materials that are currently in the production line (work-in-progress) or final products ready for sale but not yet sold.

-

Capital Goods or Plant and Machinery Held in Stock: Assets, machinery, or equipment for which ITC was claimed at the time of purchase but are now shifting to an exempt or composition usage.

Key Triggers for Filing:

-

Opting for the Composition Scheme: When a registered taxpayer decides to move from the regular tax payment scheme to the Composition Scheme under Section 10.

Need help with this? Talk to Taxottam → -

Goods/Services Becoming Wholly Exempt: When a taxable supply of goods or services becomes entirely exempt from tax under Section 11.

How is the Reversal Amount Calculated?

The calculation of the amount payable depends entirely on the nature of the stock held on the day immediately preceding the date of the change:

-

For Inputs (Raw Materials/Finished Stock): The calculation is simple. The reversal amount is equivalent to the actual ITC availed on those specific inputs based on the original purchase invoices. If invoices are unavailable, market value certified by a Chartered Accountant can be utilized.

-

For Capital Goods / Plant & Machinery: The ITC involved is calculated on a pro-rata basis. The life of capital goods is legally assumed to be 5 years (60 months) from the date of the invoice. The credit to be reversed is reduced by 5% per quarter or part thereof for the period the asset was used under the regular scheme. The remaining balance must be paid back.

Methods of Payment

Taxpayers can clear this liability using two methods through the GST Portal:

-

Electronic Credit Ledger: If you have an existing balance of valid input tax credit from other purchases, it can be used to offset this reversal liability.

-

Electronic Cash Ledger: If the credit ledger balance is insufficient, the taxpayer must generate a challan and pay the remaining balance in cash.

Essential Compliance Steps

To file GST ITC-03 smoothly, ensure you compile the following details beforehand:

-

An accurate, physically verified inventory count of inputs, semi-finished goods, finished goods, and capital goods.

-

Corresponding purchase invoices to map the exact ITC claimed previously.

-

A digital signature (DSC) or Electronic Verification Code (EVC) to sign and submit the form on the GST portal.

-

Note: If invoices are missing or special valuations are needed, a certificate from a practicing Chartered Accountant (CA) or Cost Accountant may be mandatory to validate the calculations.

Need Expert Guidance?

Determining the exact pro-rata credit for aging plant and machinery or tracking down historical invoices for semi-finished goods can be highly complex. Errors in calculating ITC reversals can lead to audit flags, interest liabilities, or penalties from the tax authorities.

Our experienced team of GST consultants can help you accurately reconcile your stock, calculate your liability under Form GST ITC-03, and file it seamlessly.

Contact Our Tax Advisers Today to ensure your business transitions remain fully compliant with the latest GST rules.

Have Questions? We're Here to Help

Get expert advice from Taxottam. Reach out to discuss your requirements.